To say the least, next Tuesday will be "interesting". In the last few months we've experienced two assignation attempts, a candidate being inserted rather than voted in through the primary process and a barrage of media, commercials and rallies by both sides. Here in the office, we have often gotten the question, "what's going to happen?" I have given a presentation entitled, "The Election And Your Money" three times since early July. The presentation's focus is on not asking the question concerning what is going to happen but rather what should I do once I know.

Quite frankly, no one knows who will be President in January at this point. However, we can prepare now for either candidate. If you would like to have a one on one discussion about your situation and whether or not either candidate's policies will affect your financial situation, please give us a call to set up a complimentary meeting over a cup of coffee. (731-285-0097)

However, I thought I would pull a few slides from the presentation as the information is general enough to share with the public. Here are a few mistakes many investors make in Presidential election years, why they make the mistakes and what you should consider doing now.

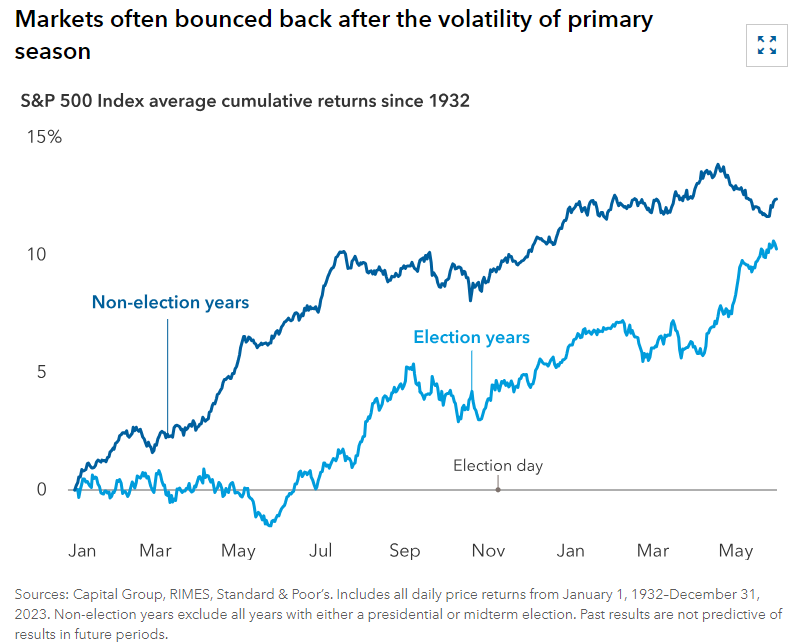

The market reacts to fear:

As you can see in the chart below, in non-election years, the market typically experiences less volatility. Uncertainty creates volatility and volatility creates fear. In election years, we experience uncertainty typically through the primaries as we don't know who "may" be leading our country. Once the primaries are over, volatility typically tones down until a few months before election day. This year has been slightly different but July was rough and there has been no shortage of hand wringing and questions by investors. The point is, this is normal. It is human nature. But unfortunately, investors tend to make drastic moves in reaction to uncertainty.

Investors sit in cash:

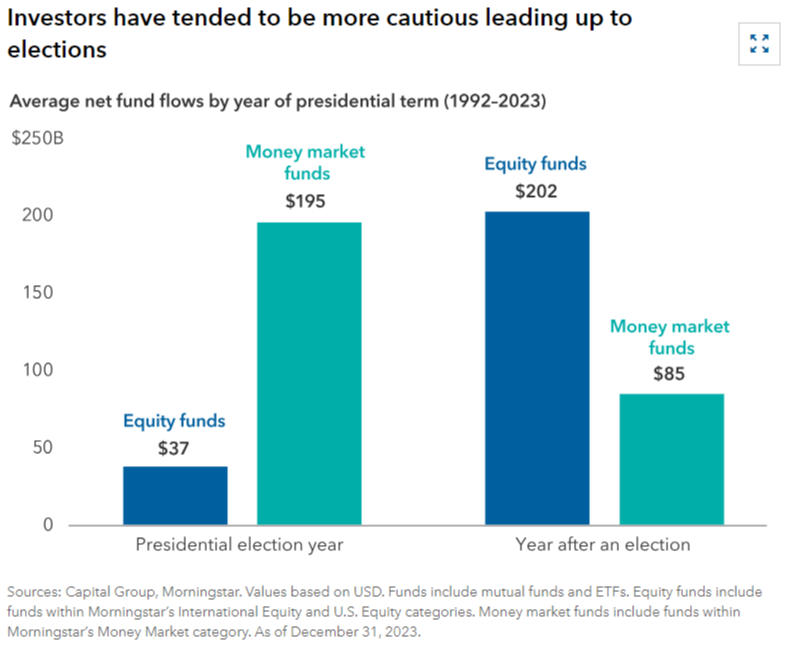

Typically, when someone is scared and uncertain about the market, they go to cash. In my career, I have seen this happen over and over. I will not make an argument over the right or wrong of that strategy here as everyone is different. However, "Going to cash" typically means you are either in the wrong asset allocation to begin with OR you don't have enough time to make up a major loss OR you are speculating. Regardless, going to cash is difficult because it involves "timing" the market. And not only are you timing when to get out, you have to time when to get back in. The emotions of fear and greed typically get involved and that is what makes it hard for the typical investor. As you can see below, during a presidential election year, investors typically go to the sidelines. And again, as you can see in the chart above, while investors sit on their hands and "wonder" if they should get back in, the market on average has gone up before, during and after the election. That "time out" can be costly to long term performance.

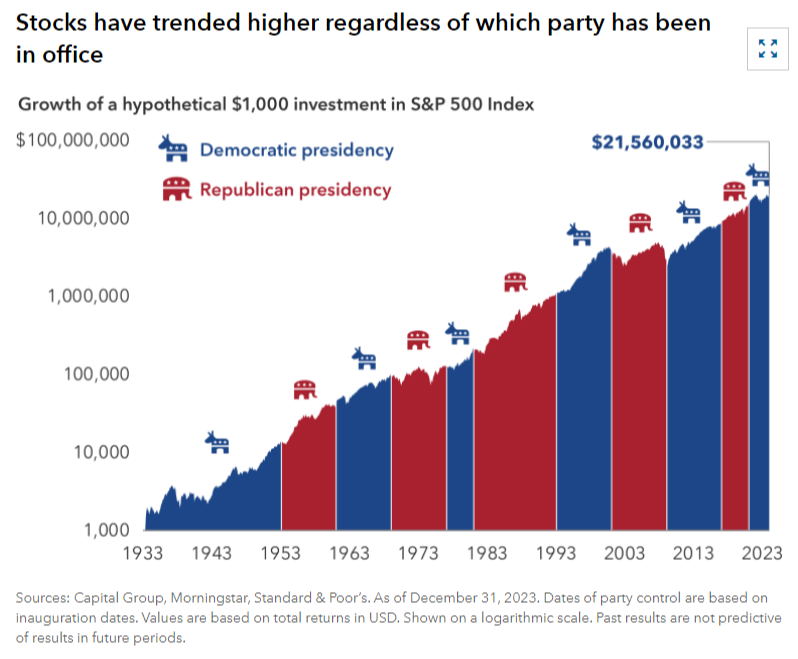

It really doesn't matter.

Blue or Red... As you can see in the chart below, the market has gone up since the 1930's under both Republican and Democratic leadership. Presidents don't make markets. Markets make presidents. And please do not get me wrong... I am not saying the market is going straight up. It doesn't. In my career, I have seen five major corrections and many short term dips. However, your chances of making money in the market go up with a longer time horizon.

Here are a few ideas to consider over the next few months. We build these into our financial plans anyway. But in election years where uncertainty is high, we all need a refresher on the basics and why they work.

What do you need?

Whether you are younger and saving for a goal such as retirement or a home, you need to define what the goal is and how much time you have to achieve it. If you are older and investing for income, how much do you need? Without defining that FIRST, you are on a trip without a map.

What is your asset allocation?

Once you know what you need and when, you can build a portfolio that matches that need. MANY times, I see investors take more OR less risk than they need. Recently, I had a prospective client bring me their 401-k statement to review for an IRA rollover. 100% of it was in U.S. Equities. This is not a good allocation for a retiree that will need this money for likely twenty five to thirty years. A major correction would change her lifestyle! On the flip side, if you have 100% of your money in a savings account earning 1% and inflation is 6%, you are losing purchasing power that you will never recover. A properly thought out allocation is crucial to managing risk and achieving your long term financial goals.

When did you rebalance?

This one is often over looked but crucial in investment management. If your allocation (for simplicity sake) started at 50% stocks and 50% bonds on January 1 and the market went up 20% this year and bonds went down 5%, your new allocation would be approximately 56% stocks and 44% bonds. In this scenario, you are taking more risk and you are one year older. Left unchecked for a period of years, you could be taking substantially more risk than you need and naturally have less time to make up a loss. This can work in the opposite direction as well. Periodically rebalancing takes the emotion out of investing by taking the "when" to buy and sell question out of the equation. This is critical to managing risk in an investment portfolio.

(If Harris wins) Who is your CPA and estate planning attorney?

There is waaaaayyyyy too much potential tax and estate policy to discuss here. But Harris' open policy is to raise taxes. This is why I say, get prepared now. Again, we do not know who will be president in January, but we do generally know how they plan to pay for the government. We are already having certain discussions with high net worth clients to prepare on how to maneuver and plan for higher taxes should Harris and a Democratic Congress be put into power. Again, if you would like to come in to discuss this over a cup of coffee to at least get an idea of whether or not you need to be concerned, please give us a call to set an appointment.

In conclusion, if a storm is coming your way, you have a choice on whether to temporarily flee or hunker down and wait it out. You do not "wonder" if the storm is going to hit. You prepare. That is what I am proposing today. Do not make drastic decisions on what MAY happen. Rather, have discussions with your financial advisor, CPA and estate planning attorney to see if you are prepared currently and if not, how to get prepared. Whether you work with us currently or not, if you need to discuss this topic further, please give us a call at your convenience.

Next blog I will be discussing "Entry Risk" and how to minimize it. This will be particularly of interest to anyone retiring soon, receiving an inheritance, selling a business/property or receiving a large sum of money in general. If you have a topic that you would like for me to write about, please email the subject to me chad@daviswealthservices.com.

Until Next Time, Cheers!